- It’s not just about US big-tech.

- Most other countries are up, and a dozen markets are up even more than the US.

- Why are booms & busts global?

- Is it time for the next big sell-off?

If you believe the media hype surrounding the share rally this year, you would get the impression that it’s mainly a US big-tech rally. It’s all about the US ‘Magnificent-7’, right? The implication is that if you have not been in the US share market, you have missed out. But is that true?

As usual, the media hype distorts the facts. This year’s share rally is not just about the US. It has been a broad global rally. 80% of country share markets are up this year, and more than a dozen countries are up by even more than the US.

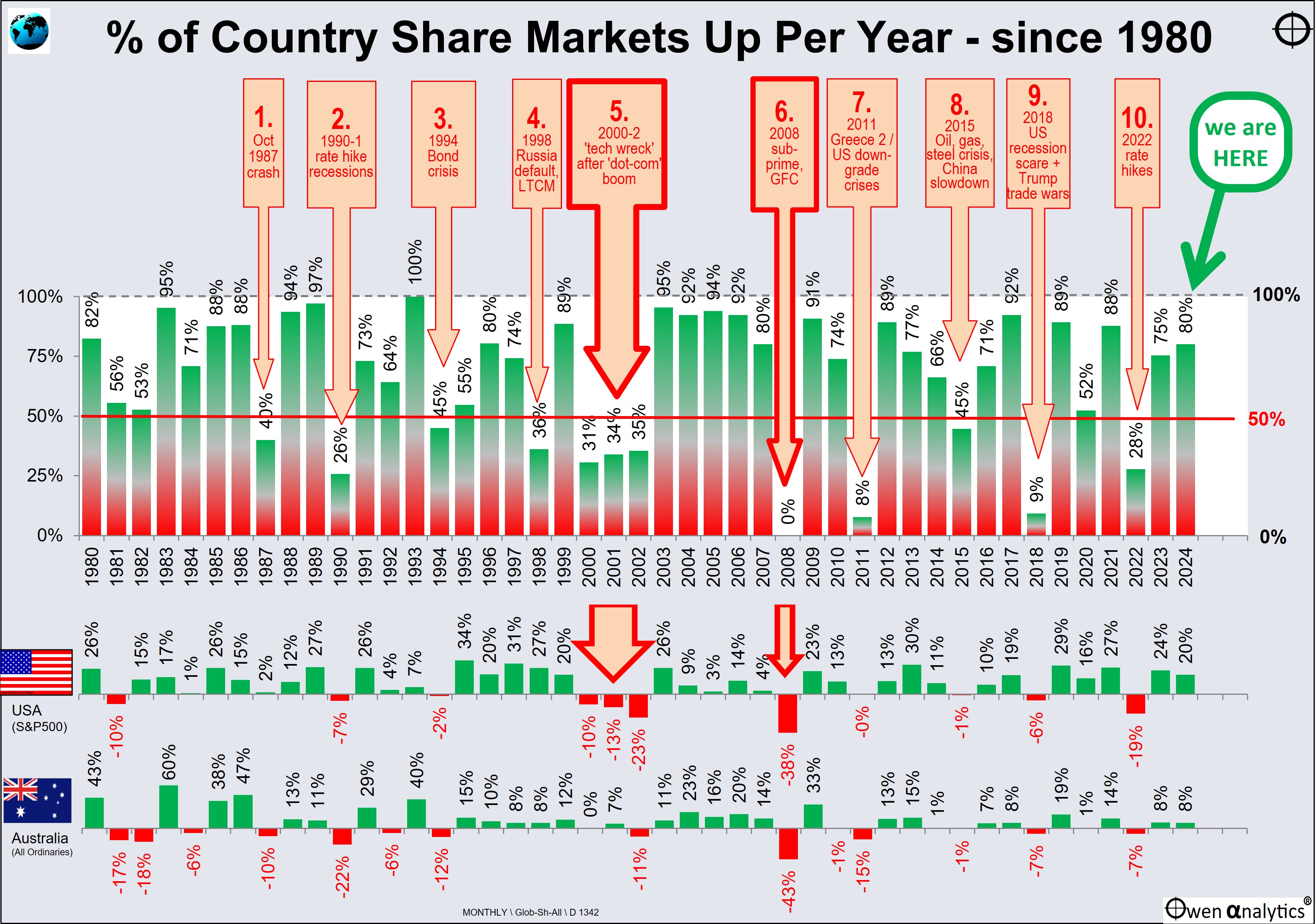

Today’s chart shows the percentage of country share markets that posted positive gains each year since 1980, out of the 60+ countries I cover. Data in the chart is up to the end of October, so it is before the strong rally following the US elections in November.

This year, 80% of share country share markets are up to the end of October. This is better than the overall average year when around two thirds of share markets are up.

Of the 65 country share markets in the chart, the US market is ranked 14th best so far in 2024. Thirteen 13 other countries I cover have done even better than the US market this year, including: Pakistan +42%, Taiwan +27%, Cyprus +44%, Egypt +23%, Kenya +27%, Nigeria +31%, Slovenia, +30%, and a handful of others.

US dominates

The lower section of the chart shows the annual gains or losses in the US market (S&P500 index). Whenever the US market has a bad year (red negative bars on the US bar chart), it drags down most other markets with it. Conversely, whenever the US market has a good year, most other global share markets also do well.

Why? Mainly because global fear is contagious, and global confidence is contagious. Investors are emotional animals, driven mainly by fear and greed, not by rational logic.

Australia follows the US, with local variations

The bottom section shows annual gains/losses on the Australian share market (All Ordinaries index) each year. The local market follows the US, with minor local variations along the way. Every year when the US market was down, the local market was also down, regardless of local conditions, local pricing or local events.

Only one year when all share markets were up

There has only been one year when all share markets were up together. That was in 1993, in the global rebound from the deep early-1990s recessions.

Global sell-offs

In the past 45 years shown on this chart, there have been 12 years when most share market posted losses. These occurred in 10 global sell-offs – highlighted by the pink arrows in upper section of the chart. I will comment on two of these global sell-offs in particular:

2008 GFC

Number 6 – the 2008 global financial crisis. I highlight it here because it was the only year when every major share market was down (0% were positive).

The crisis started in the US with the collapse of the US housing market. That, in turn, triggered the collapse of the US sub-prime credit derivatives market, then the US banking system, then contagion very quickly spread to banks around the world. Fears of a global banking/economic collapse led panicking investors to dump not just bank shares but all shares, everywhere.

The broad US market was down -38% in 2008, but the Australian market fell by -43%. This was even worse than the US market, even though Australia didn’t have a housing crisis, didn’t have a sub-prime derivatives crisis, didn’t have a banking crisis, and didn’t even have an economic recession! Why? Because when global investors panic, they dump everything, everywhere, regardless of local conditions or local pricing.

The good news is that when (not if) the current boom ends, it will probably not trigger a global banking crisis like the GFC.

2000-2 tech wreck

The second big sell-off I highlight here is Number 5 – the 2000-2 ‘tech-wreck’ that followed the incredible late-1990s ‘dot-com’ boom. It is similar in many ways to the current cycle we are in at the moment.

The 2000-2 ‘tech wreck’ was the only sell-off when the majority of global share markets were down for more than a single year. The broad global sell-off ran for three consecutive years, which is most unusual. (The only other three-year global bear market was in 1929-31).

In the 2000-2 ‘tech-wreck’, most of the pain was in US tech stocks, which dragged the NASDAQ index down 90% overall. But it wasn’t just a tech sell-off. When a speculative tech boom collapses, it affects everything, not just tech stocks. When the 1990s tech boom eventually collapsed, it was enough to drag the overall S&P500 index down by -10% in 2020, then another -13% in 2001, and another -23% in 2002. It also triggered a general US and global recession in 2001.

Australia only had a very minor tech boom in the late 1990s (believe it or not our two largest ‘tech’ stocks were Telstra and News Corp!) but our market still posted very poor returns in 2000, 2001, and 2002. Same reason - global fear is contagious, regardless of local conditions or pricing.

End of the current boom?

Although current over-pricing affects is mainly confined to US tech stocks, when (not if) the current boom collapses, it will probably drag down most other sectors, and most other share markets around the world, and probably also trigger broad economic recessions.

On a positive front, the current level of over-pricing is only about half as severe as it was at the end of the 1990s. The 1990s tech boom ran about twice as long, and about twice as high as the current boom, so far.

Booms always collapse, but they don’t collapse because or when they are over-priced. They often run a lot longer and a lot higher than logic or most people expect.

The trigger or combination of triggers is different each time.

Timing?

I have been over-weight US and global shares in the current boom, and I still am, despite over-pricing. Why?

In the words of investment guru Peter Lynch in his must-read classic - ‘One Up on Wall Street’ (1989, Simon & Schuster, NY ) -

‘Far more money has been lost by investors trying to anticipate corrections, than lost in the corrections themselves’

See also:

For my current views on asset classes and asset allocations - see:

'Till next time - happy investing!